Tenzing works with more than 40 insurance providers, which means we can offer more than 10,000 different policy options. The price can range from a few hundred dollars a year to more than $10,000. Why such a disparity between bargain and deluxe?

Do you know what an insurance premium is? It’s simply the annual amount you pay for the policy, whether you actually pay annually or on a more frequent basis.

Let’s explore some of the most important factors that determine your premium:

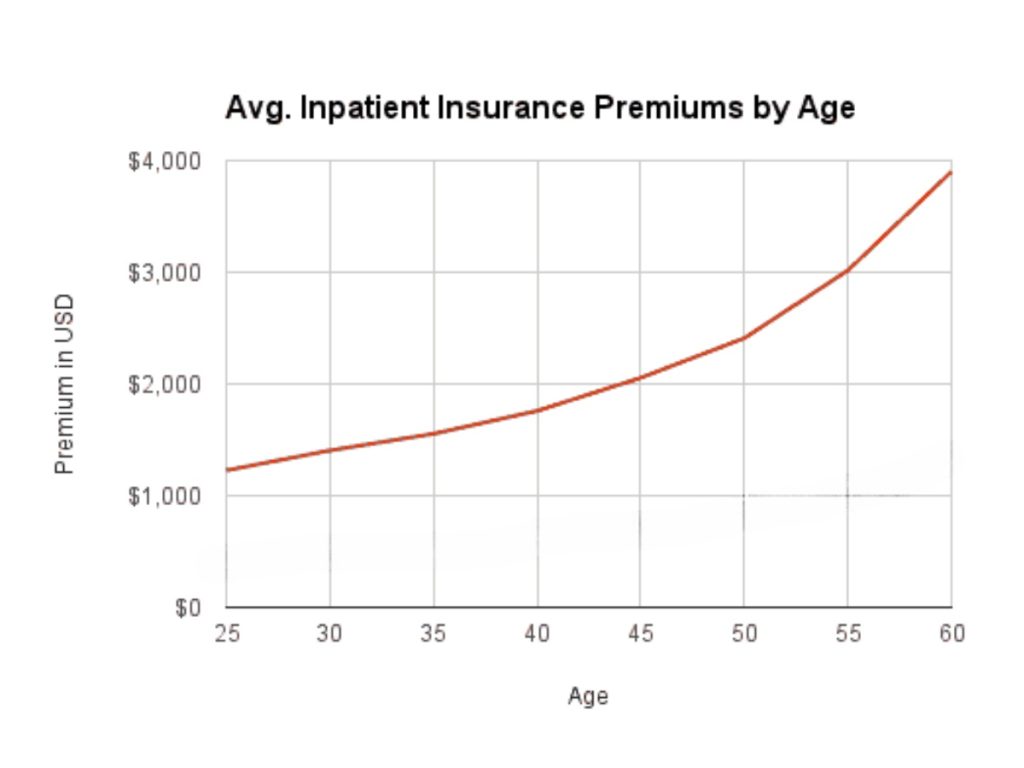

1. Age

The simple fact is that our health declines as we age. A major illness in one’s 40’s is an outlier, but the reality is that everyone eventually succumbs to some medical condition. Since insurance policies cover these medical costs, older people are a higher risk for the insurers and thus require higher premiums. Conversely, younger people represent lower risk and their premiums are lower.

One result of these dynamics is that the cost of a policy will rise faster for older customers. This is true for new and existing customers equally, since premiums are subject to annual increases.

It’s also important to note that some providers restrict the age for accepting new applicants, usually at age 60 or 65. There are still options if you’re 65+, just fewer and more expensive.

2. Coverage Area

All insurance providers define the area where policyholders have their coverage. The cost of healthcare in the region of coverage will have a significant impact on the premium. Most insurers in Southeast Asia offer some version of four main coverage areas:

Residence country only, such as Vietnam only or Thailand only.

Southeast Asia, whether using the list of ASEAN countries or a variation: Brunei, Burma (Myanmar), Cambodia, Timor-Leste, Indonesia, Laos, Malaysia, the Philippines, Singapore, Thailand, Vietnam. Many providers who offer Southeast Asia coverage exclude Singapore because the cost of healthcare in Singapore is so much higher.

Worldwide, but excluding the USA (or other countries): The cost of healthcare in the USA is astronomical compared to most countries, so providers often exclude it from an otherwise worldwide coverage area. Other countries may get the same treatment, such as Canada, the Caribbean, Singapore, Hong Kong, Switzerland.

Worldwide. A truly worldwide plan is relatively rare, but they are available. You’ll pay extra for the additional coverage.

Emergency coverage: most international insurance policies include some coverage in the excluded countries, but only for emergencies and often for a limited amount.

3. Benefits

All international health insurance policies have inpatient coverage as their foundation. The inpatient benefit takes care of the major medical incidents, the ones that require hospitalization.

In addition, there are add-on benefits you can choose for an additional cost, including outpatient, which covers you for everyday treatments at a doctor’s office or clinic. This is a highly utilized benefit, which tends to drive up its cost to roughly double that of an inpatient-only policy.

Maternity, Dental and Vision benefits are typically available too.